Chapter 2: Why Switch? Evaluating the Value of Switch Candidates

16

the remaining prescription patients (who have

low generic co-pays) to OTC consumers. It also

is more difficult to switch Rx volume to OTC

when the switch is a “partial” switch, and some

indications remain available by prescription, such

as was the case with Flonase. Taking a deeper

look at the allergy category, the trends to source

OTC volume from existing and new OTC users

have intensified. Table 2-4 provides data on the

source of volume for many recent allergy Rx-to-

OTC switches.

Nonetheless, there were enough new

sufferers in the allergy category that the intro-

duction of INS in 2013 brought enough new

users to the OTC market to prevent sales of

non-sedating antihistamines from declining

(although behind-the-counter combination

products of non-sedating antihistamines with

the decongestant pseudoephedrine did decline

slightly). One thing that the INS brands did

well was to encourage use before the start of the

allergy season as a preventative measure, thus

getting allergy sufferers to treat for more days in

the allergy season. Table 2-5 demonstrates that

the launch of INS brands did not steal category

share from NSAs, but rather grew the overall

allergy category.

With four OTC allergy brands in the US

exceeding $200 million in sales, another new

product in the OTC allergy category would

need to either bring significant prescription sales

volume, create a reason for existing OTC users to

switch brands, or convince non-treaters to begin

treating. In August 2018, Perrigo announced a

deal with Merck and Co., Inc. to switch Nasonex

(mometasone) to OTC.8 Once a blockbuster pre-

scription drug with sales in excess of $1 billion,9

generic versions of Nasonex have been available

since 2016.10 It will be interesting to see what

happens to Nasonex based on the order of entry

theory above. Unless Nasonex can secure a differ-

entiating claim, such as allergy prevention, it may

be hard for this brand to be successful in spite of

its latent equity.

While the allergy category is large and grow-

ing in size, thus providing favorable dynamics for

multiple successful switches, other categories are

smaller and declining, creating obstacles for com-

panies considering new switches. One of these

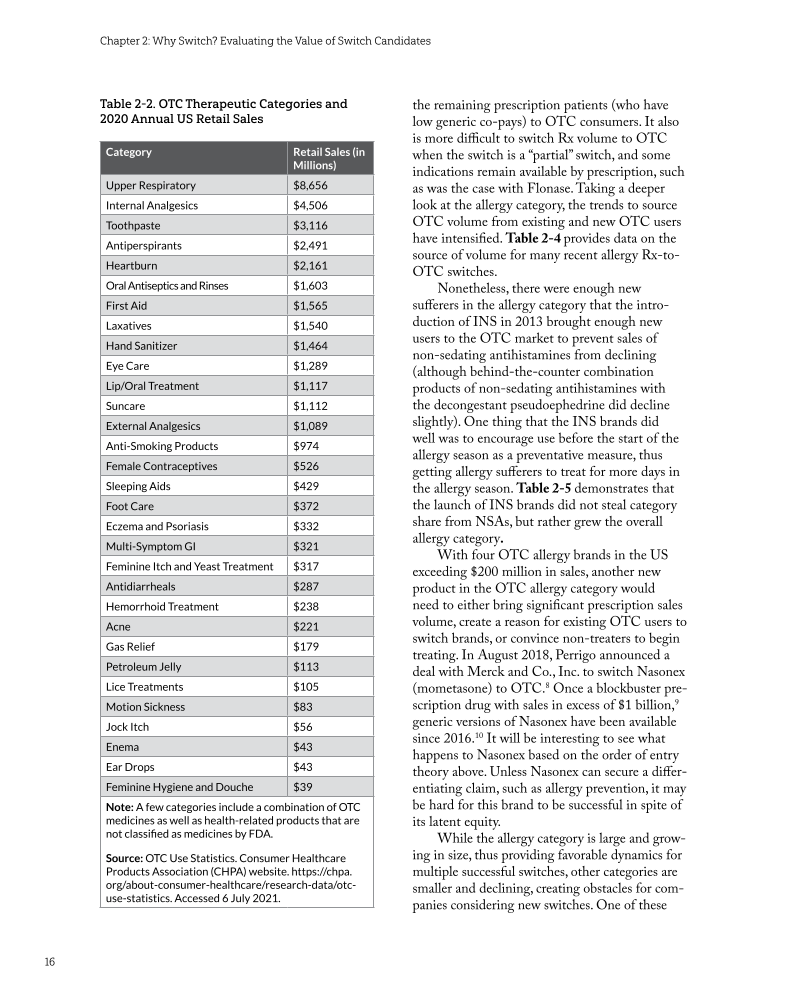

Table 2-2. OTC Therapeutic Categories and

2020 Annual US Retail Sales

Category Retail Sales (in

Millions)

Upper Respiratory $8,656

Internal Analgesics $4,506

Toothpaste $3,116

Antiperspirants $2,491

Heartburn $2,161

Oral Antiseptics and Rinses $1,603

First Aid $1,565

Laxatives $1,540

Hand Sanitizer $1,464

Eye Care $1,289

Lip/Oral Treatment $1,117

Suncare $1,112

External Analgesics $1,089

Anti-Smoking Products $974

Female Contraceptives $526

Sleeping Aids $429

Foot Care $372

Eczema and Psoriasis $332

Multi-Symptom GI $321

Feminine Itch and Yeast Treatment $317

Antidiarrheals $287

Hemorrhoid Treatment $238

Acne $221

Gas Relief $179

Petroleum Jelly $113

Lice Treatments $105

Motion Sickness $83

Jock Itch $56

Enema $43

Ear Drops $43

Feminine Hygiene and Douche $39

Note: A few categories include a combination of OTC

medicines as well as health-related products that are

not classified as medicines by FDA.

Source: OTC Use Statistics. Consumer Healthcare

Products Association (CHPA) website. https://chpa.

org/about-consumer-healthcare/research-data/otc-

use-statistics. Accessed 6 July 2021.

16

the remaining prescription patients (who have

low generic co-pays) to OTC consumers. It also

is more difficult to switch Rx volume to OTC

when the switch is a “partial” switch, and some

indications remain available by prescription, such

as was the case with Flonase. Taking a deeper

look at the allergy category, the trends to source

OTC volume from existing and new OTC users

have intensified. Table 2-4 provides data on the

source of volume for many recent allergy Rx-to-

OTC switches.

Nonetheless, there were enough new

sufferers in the allergy category that the intro-

duction of INS in 2013 brought enough new

users to the OTC market to prevent sales of

non-sedating antihistamines from declining

(although behind-the-counter combination

products of non-sedating antihistamines with

the decongestant pseudoephedrine did decline

slightly). One thing that the INS brands did

well was to encourage use before the start of the

allergy season as a preventative measure, thus

getting allergy sufferers to treat for more days in

the allergy season. Table 2-5 demonstrates that

the launch of INS brands did not steal category

share from NSAs, but rather grew the overall

allergy category.

With four OTC allergy brands in the US

exceeding $200 million in sales, another new

product in the OTC allergy category would

need to either bring significant prescription sales

volume, create a reason for existing OTC users to

switch brands, or convince non-treaters to begin

treating. In August 2018, Perrigo announced a

deal with Merck and Co., Inc. to switch Nasonex

(mometasone) to OTC.8 Once a blockbuster pre-

scription drug with sales in excess of $1 billion,9

generic versions of Nasonex have been available

since 2016.10 It will be interesting to see what

happens to Nasonex based on the order of entry

theory above. Unless Nasonex can secure a differ-

entiating claim, such as allergy prevention, it may

be hard for this brand to be successful in spite of

its latent equity.

While the allergy category is large and grow-

ing in size, thus providing favorable dynamics for

multiple successful switches, other categories are

smaller and declining, creating obstacles for com-

panies considering new switches. One of these

Table 2-2. OTC Therapeutic Categories and

2020 Annual US Retail Sales

Category Retail Sales (in

Millions)

Upper Respiratory $8,656

Internal Analgesics $4,506

Toothpaste $3,116

Antiperspirants $2,491

Heartburn $2,161

Oral Antiseptics and Rinses $1,603

First Aid $1,565

Laxatives $1,540

Hand Sanitizer $1,464

Eye Care $1,289

Lip/Oral Treatment $1,117

Suncare $1,112

External Analgesics $1,089

Anti-Smoking Products $974

Female Contraceptives $526

Sleeping Aids $429

Foot Care $372

Eczema and Psoriasis $332

Multi-Symptom GI $321

Feminine Itch and Yeast Treatment $317

Antidiarrheals $287

Hemorrhoid Treatment $238

Acne $221

Gas Relief $179

Petroleum Jelly $113

Lice Treatments $105

Motion Sickness $83

Jock Itch $56

Enema $43

Ear Drops $43

Feminine Hygiene and Douche $39

Note: A few categories include a combination of OTC

medicines as well as health-related products that are

not classified as medicines by FDA.

Source: OTC Use Statistics. Consumer Healthcare

Products Association (CHPA) website. https://chpa.

org/about-consumer-healthcare/research-data/otc-

use-statistics. Accessed 6 July 2021.